Economic Data Surprise Index Shows Continued Weakness

Today we get

another glimpse into the behind-the-scenes machinations of the “data dependent”

Federal Open Market Committee (FOMC) with the

release of the minutes from the April 26-27 meeting.

While the Fed

has a dual mandate of maximum employment and price stability, lately there has

been considerable discussion about the how much the Fed should let global

considerations factor into Fed policy.

Clearly, the pace of economic growth in China or the

stability of euro zone has a significant downstream effect on economic activity

in the United States. Additionally, with

48% of revenues from the S&P 500 companies coming from international

markets, policy formulation in an increasingly interconnected global economy is

becoming more complicated with each advance in technology, communications and

logistics.

Given this

backdrop, just how does the data look?

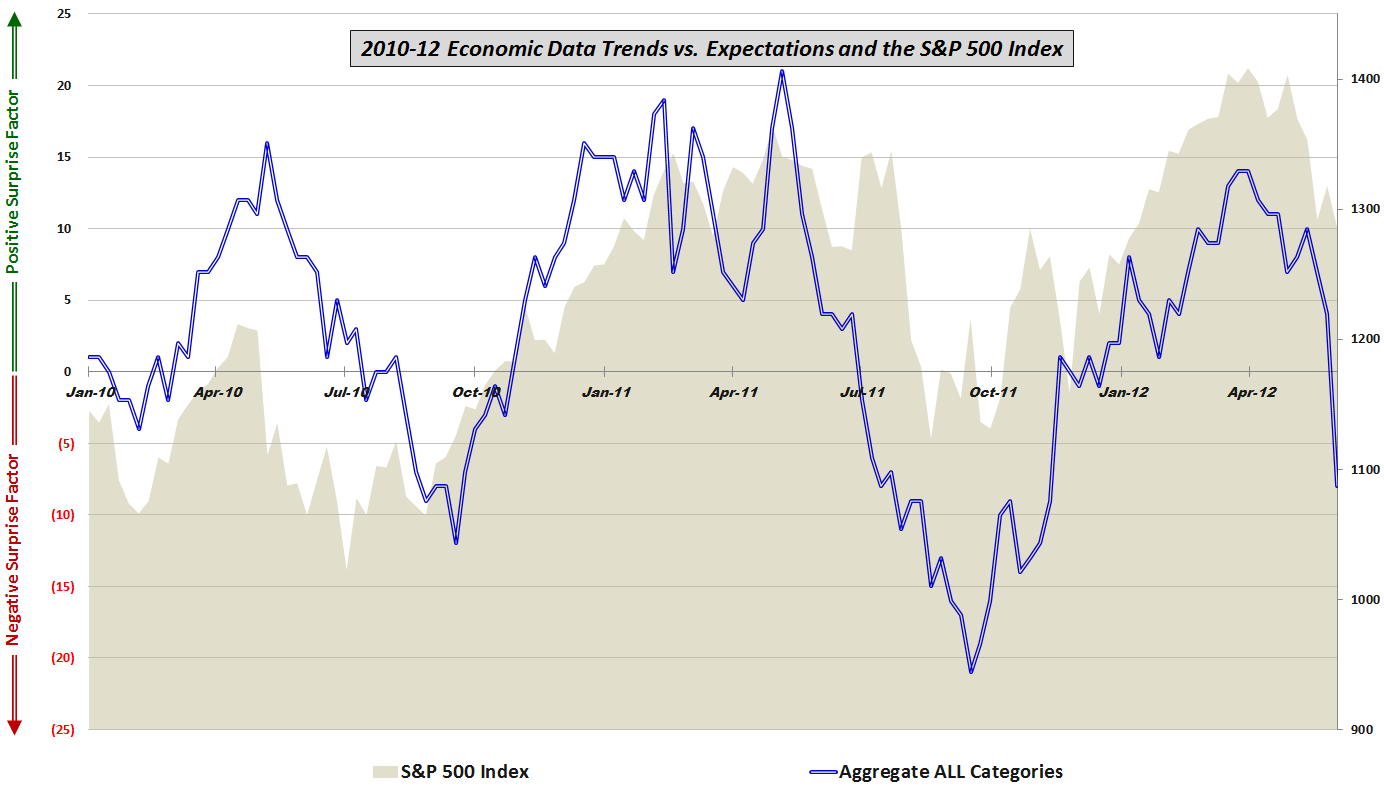

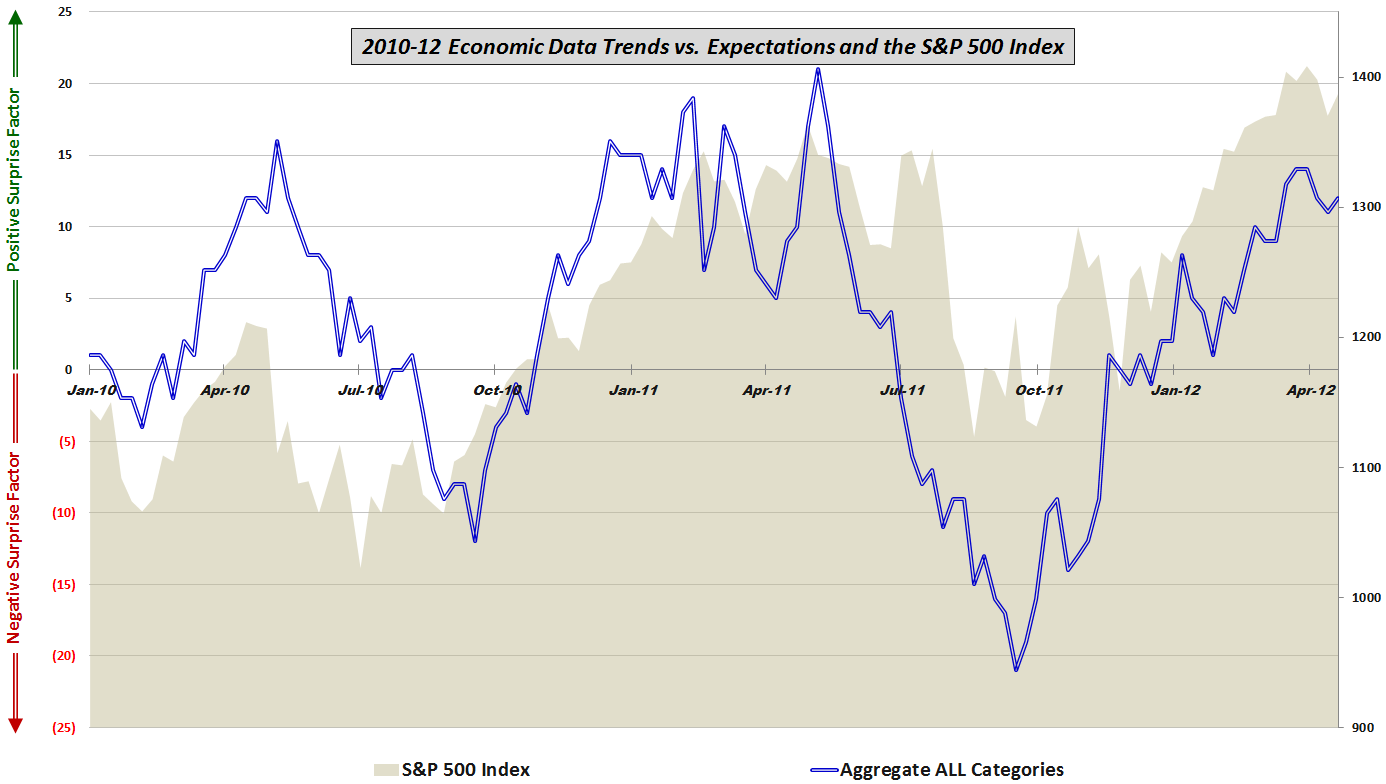

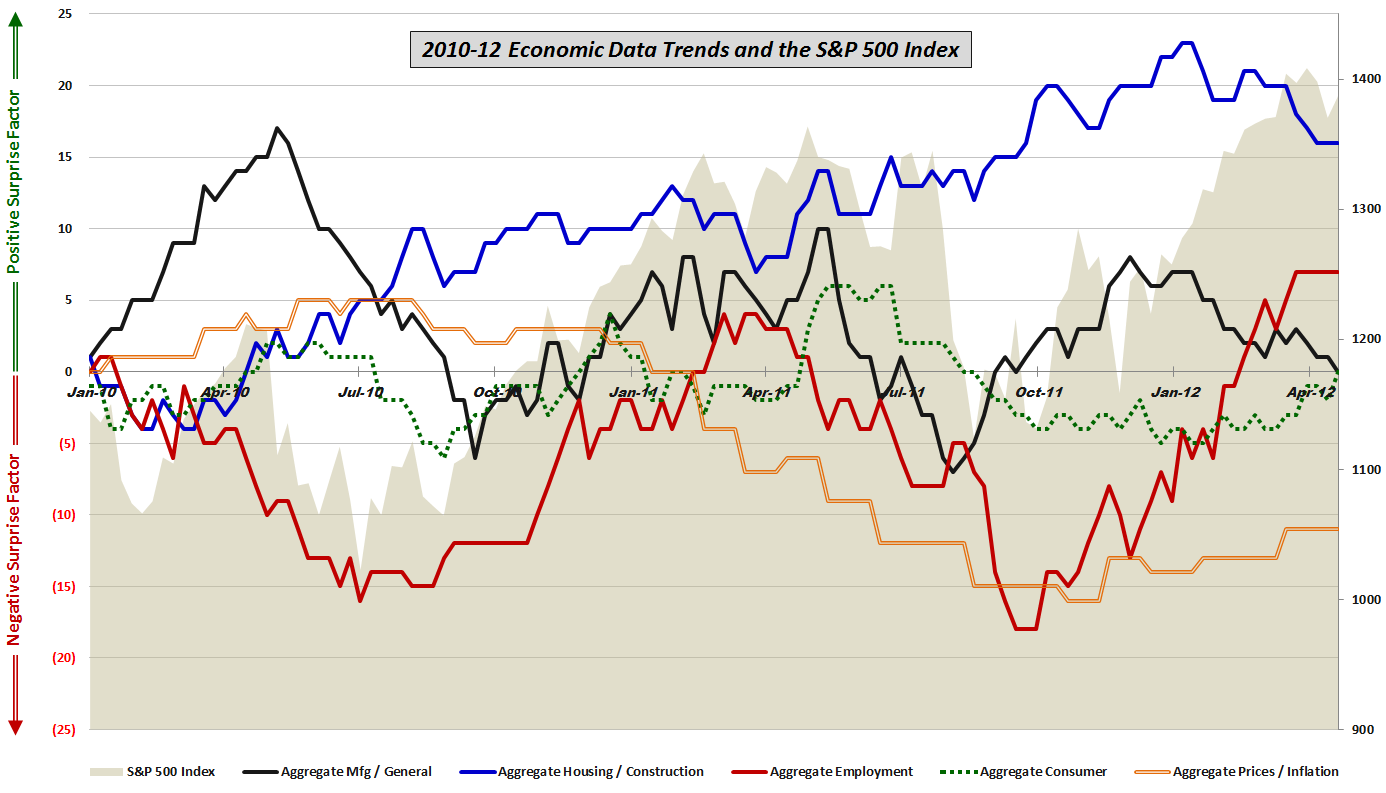

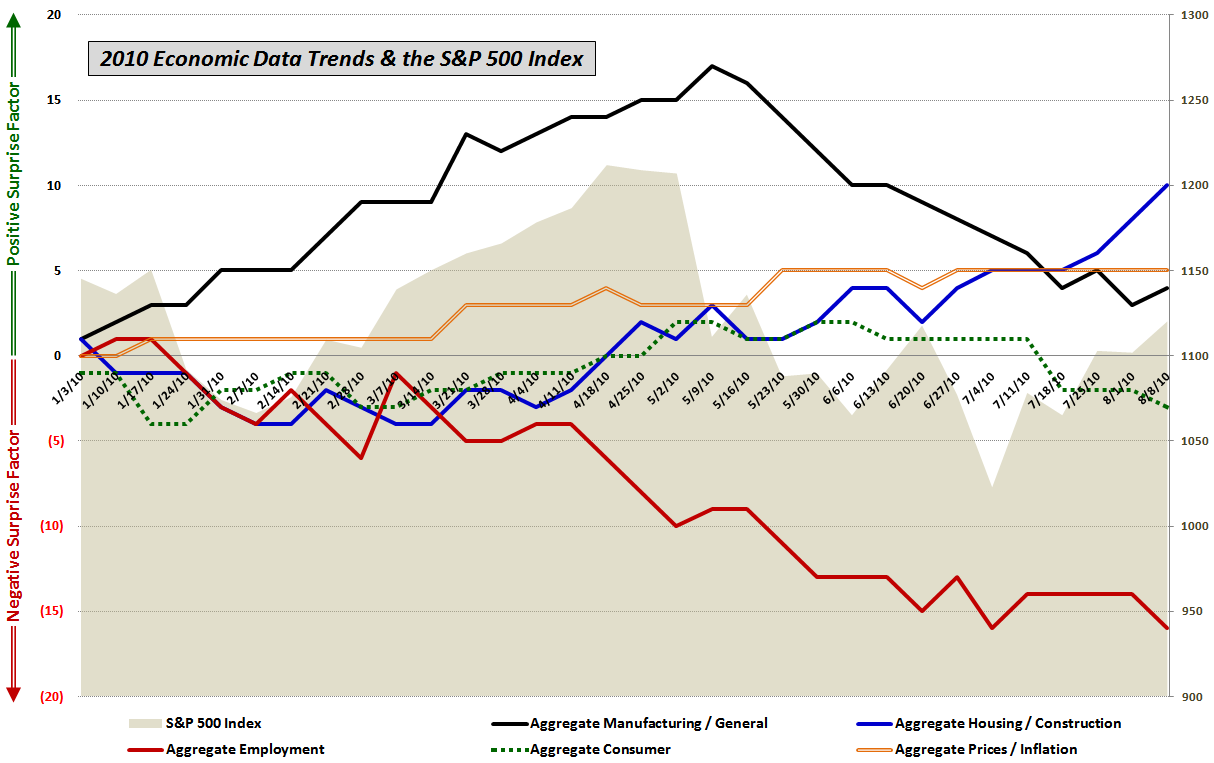

For the past seven years I have been publishing an economic data

surprise index that aggregates U.S. economic data relative to consensus

expectations across areas such as employment, the

consumer, housing/construction,

manufacturing and inflation. The chart

below aggregates data across all these areas and shows data peaking relative to

expectations during October 2014. Since

that peak, however, economic data relative to expectations deteriorated

sharply, falling to an all-time low during the middle of January 2016 that was

matched again at the end of last month.

[source(s): VIX and More]

If the Fed is

indeed data dependent, then there is no avoiding the conclusion that aggregate

data relative to expectations has been a disaster for the past 1 ½ months. There are some signs of stability forming in

the current environment and clearly the strength of the dollar and the

price of crude

oil will have a great deal to say about economic data going forward. Then again, international events such as the Brexit vote and

the evolution of negative

interest rate policies of central banks across the globe may trump all

domestic U.S. economic data.

[Readers who

are interested in more information on the component data included in this

graphic and the methodology used are encouraged to check out the links below.

For those seeking more details on the specific economic data releases which are

part of my aggregate data calculations, check out Chart

of the Week: The Year in Economic Data (2010).]

Related posts:

- Stocks and Economic Data Continue to Move in Opposite Directions

- The Economic Data Cliff

- Worst Post-2009 Week in Economic Data Relative to Expectations

- Stocks and Economic Data on Upswing Despite Disappointing Manufacturing and Housing Numbers

- Economic Data vs. Expectations: Stocks and Employment Data Rallying Since October

- Economic Data: Divergence or Confirmation for Stocks?

- Aggregate View of U.S. Data vs. Expectations

- How Good Has the U.S. Data Been Lately?

- Economic Data Not Supporting Gloom and Doom Forecasts – At Least for Now

- Economic Data Relative to Expectations and Stock Prices

- Continued Lackluster Data vs. Expectations

- Economic Data Frozen Until Next Thursday

- More Upticks in Economic Data vs. Expectations

- Economic Data Trends Improving

- Chart of the Week: Updated Economic Data Trends

- Economic Data Trends in Advance of Nonfarm Payrolls

- Trends in Economic Data Relative to Expectations

Disclosure(s): none