VIX Futures Margin Requirements to Increase After Today’s Close

A number of readers have expressed concern to me privately about today’s increase in the VIX futures margin requirements. The current margin requirements are detailed at the CFE Margins splash page, while the new margin requirements were outlined in CFE Regulatory Circular RG13-019 on Tuesday and were just updated on the CFE (CBOE Futures Exchange) web site here.

Perhaps the most critical of the changes is the substantial increase in margin requirements for spread positions. The current initial margin requirement for a spread is $625 - $1250, with the variation due to the number of months involved in the spread. The maintenance margin for these positions is currently $500 - $1000. After today’s close, the initial margin requirement jumps to $2860 - $4015, with the maintenance margin rising to $2700 - $3650.

For those VIX futures spread traders out there – and I’d imagine that includes just about all VIX futures traders – this is an increase of 5-6 times the current margin requirement and has the potential to trigger some forced liquidations. If you have any concerns about your margin position going into tomorrow’s trading day, I urge you to take the balance of today’s trading session to make the appropriate adjustments.

As best as I can tell, quite a few VIX spread traders are not aware of these margin requirements changes, which could only add to any potential market dislocation.

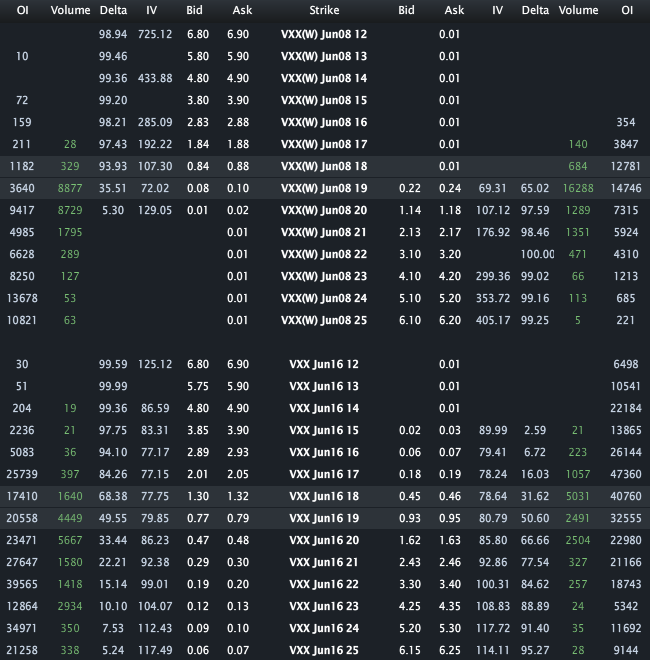

Of course the VIX futures are also an essential ingredient in the VIX ETPs, notably VXX, which also has weekly options expiring tomorrow…so depending upon how much impact the new margin requirements have on the VIX futures market, VXX, XIV, UVXY, TVIX and their associated options (as well as the full stable of VIX ETPs) could be influenced by tomorrow’s market action.

In addition to the potential issues related to the VIX futures market tomorrow, there are a number of broader issues that are related to the margin requirements. For starters, the CFE used to set margin requirements for the VIX futures. This responsibility recently moved to the OCC, which uses a large-scale Monte Carlo-based risk management methodology, known as System for Theoretical Analysis and Numerical Simulations (“STANS”) that is said to evaluate approximately 7,000 risk factors. Today’s margin requirements change is the first instance in which the OCC made the determination (presumably after STANS crunched the numbers for rising volatility across a wide variety of asset classes) to change margin requirements and essentially directed the CFE to implement this change. Recognizing that this was the first OCC-driven margin requirements change, the CFE issued the regulatory circular referenced above to explain what was happening. Going forward, no such regulatory circular is likely to be issued when there are changes to margin requirements. Instead, traders are expected to learn about changes in margin requirements by visiting the CFE Margins page each morning. This raises another question: if traders think two days’ notice via a regulatory circular is not sufficient notice for margin requirement changes, I can only imagine how they will react when that notice is of the same-day variety.

Of course STANS and the OCC can change margin requirements at any time, but if the VIX futures markets do not operate with their usual efficiency tomorrow and some traders are subject to forced liquidations of relatively illiquid back month legs because they were not aware that margin requirements were about to increase by a factor of five or six, then perhaps it is time to think about some other ways that changes in margin requirements can be implemented and communicated.

Related posts:

- VIX ETP Performance in 2012

- Monitoring VIX Futures and Their Impact on VIX ETPs

- VIX Futures Brokers

- Why VXX Is Not a Good Short-Term or Long-Term Play

- VXX Calculations, VIX Futures and Time Decay

Disclosure(s): long VXX, long XIV and short UVXY at time of writing; the CBOE is an advertiser on VIX and More