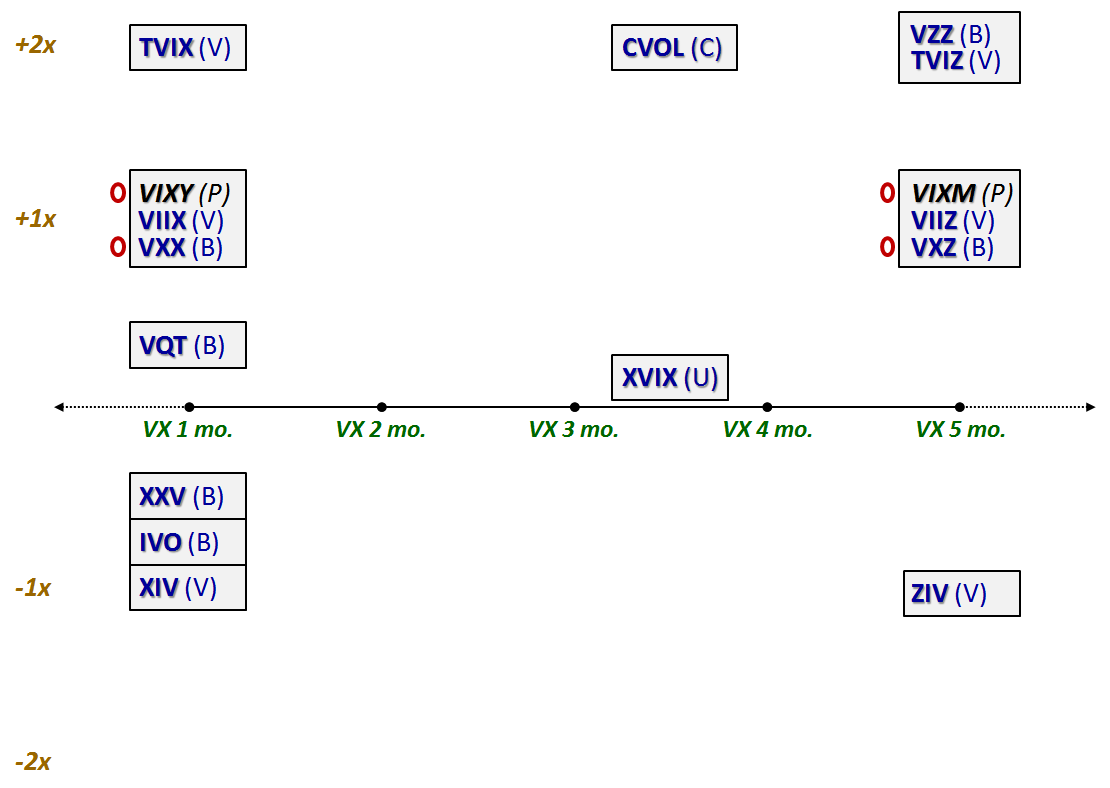

UVXY Dominates VIX ETPs By Dollar-Weighted Volume

At various times in the 13-year history of VIX ETPs there have been as many of 30+ different versions of these VIX-based products on the market. Initially, it was the +1x VXX that dominated the space, later supplanted by the +2x TVIX and then the -1x XIV as the top dog. All three of these products have run into various issues (see VIX ETPs – What Can Go Wrong?), with XIV dead, TVIX relegated to irrelevance and trading by appointment on the pink sheets as TVIXF and VXX currently wounded by regulatory issues (Barclays Suspends Creation Units for VXX).

In the wake of all this carnage, which products are still viable? A month ago I would probably have argued that VXX was the most important product in the space, but with VXX’s creation unit troubles, the +1.5x UVXY ETF from ProShares is the clear market share leader, with 63.3% of the dollar-weighted volume in the VIX ETP product space. The ProShares -0.5x SVXY ETF has the second highest dollar-weighted volume in the space at 19.4% and in third place at 9.8% is the +1.0x VIXY ETF. VXX from Barclays has fallen to fourth place at 5.8%. For now, the VIX ETP space is dominated by the ProShares product suite. The two new kids on the block, the +2.0x UVIX and the -1.0x SVIX from Volatility Shares are gaining some traction, but still have only 0.7% dollar-weighted volume share.

In the graphic below I show the dollar-weighted volume as of yesterday’s data. Note that the top six products all have a weighted-average maturity of one month while the two laggards, VIXM and VXZ, both have a weighted-average maturity of five months.

[source(s):

Yahoo, VIX and More]

Further Reading:

UVIX

and SVIX Join the VIX-Based ETP Landscape

VIX

ETPs – What Can Go Wrong?

Successful

Launch for SVIX and UVIX

VIX

ETPs Flash Some Green in 2016

Every

Single VIX ETP (Long and Short) Lost Money in 2015

Performance

of VIX ETPs During the Recent Debt Ceiling Crisis

Expanded

Performance of Volatility-Hedged and Related ETPs

Performance

of Volatility-Hedged ETPs

Performance

of VIX ETP Hedges in Current Selloff

Slicing

and Dicing all 31 Flavors of the VIX ETPs

Charting

the Assets of the Volatility-Based ETPs

For those who

may be interested, you can always follow me on Twitter at @VIXandMore

Disclosure(s): net short VXX, UVIX and UVXY, net long SVIX at

time of writing