Now Sixteen Volatility ETPs, Four of Which Are Optionable

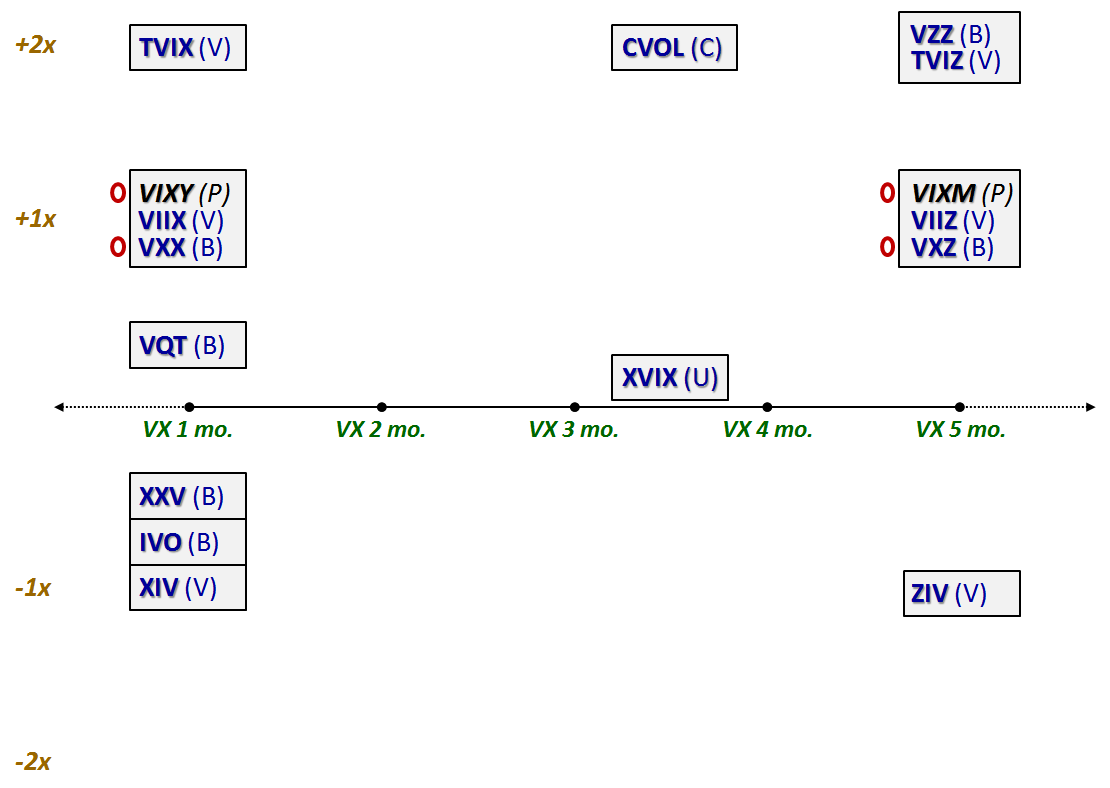

The graphic below is part of my ongoing effort not only to maintain a list of all the volatility-based exchange-traded products, but present them in a manner which helps to highlight the distinctions among these products.

Since I last updated this picture, in early December, three new VIX-based ETPs have entered the fold. Two of these are the first VIX-based ETFs and also represent the first products in this space from industry heavyweight and leveraged/inverse ETF heavyweight ProShares:

ProShares has also been fortunate in that as of this week options are now being offered on VIXY and VIXM, making these only the third and fourth optionable volatility-based ETPs, following in the footsteps of VXX and VXZ. Note that all four optionable ETPs have a red O preceding their ticker.

The third new product to be launched in the past month is the iPath Inverse January 2021 S&P 500 VIX Short-Term Futures ETN, which trades under the ticker IVO. The launch of this ETN apparently confused some observers, but is likely an attempt by Barclays to come up with an ETF that does a better job of tracking the inverse of VXX. My concern is that over time IVOs ability to mirror changes in VXX will undergo the same dilution that happened to XXV. It is possible that Barclays will periodically trot out newer versions of XXV and IVO, but until then, I see these two products as performing more like a fractional inverse ETN than XIV. For this reason, I have put XXV and IVO in separate boxes in the one month -1x space to reflect this important distinction (see Shorting VXX and Long XXV or XIV for more details.)

There are several other small changes in this chart, including moving XVIX closer to the neutral volatility line to reflect the fact that on average the long and short volatility components of this ETN net out to a very limited exposure to volatility and more direct exposure to the VIX futures term structure.

With sixteen volatility-based ETPs available for trading and options on four of those, it is not an exaggeration to say that the number of possible volatility strategies and trades is limited only by the imagination.

Related posts:

- Two More VIX ETNs Make it a Baker’s Dozen

- Impressive Launch for Sextet of New Volatility ETNs from VelocityShares

- VelocityShares Jumping in to VIX ETP Space with Leveraged and Inverse Products

- The Evolving VIX ETN Landscape

- Interesting New Leveraged Volatility ETN Coming from Citi

- Shorting VXX and Long XXV or XIV

- Ways to Turn Volatility into an Asset Class (Barron's)

Disclosure(s): short VXX; long XIV, VXZ and XVIX at time of writing