Event Risk, Event Theta and the Next Week

Weekends pose an interesting set of problems for the investor/trader, particularly when there is an ongoing crisis or a reasonable risk that a new crisis lurks around the corner. Today we have a perplexing situation in which there is both an old crisis (government shutdown) and a new crisis just around the corner (debt ceiling limit), as well as the increasing likelihood that the two of these are going to merge into one bigger crisis.

How should an investor think about this situation? First, they need to form some opinions about event risk, including a range of scenarios from a quick and comprehensive resolution of the government shutdown and the debt ceiling to prolonged gridlock that results in the U.S. defaulting on its obligations. The fun part is assigning probabilities to these scenarios, coming up with a probability weighted view of the future and making (semi-)rational decisions about portfolio protection and speculative opportunities after considering risk and potential reward. Sounds like a snap, doesn’t it?

Some investors may not fully appreciate that event risk or event volatility is a two-sided sword. Sure, there is risk that many of us have once again overestimated a bunch of elected lemmings officials and their ability to act in the best interests of their country and in so doing reprise those wonderful memories from August 2011, but there is also the risk that some progress – or even a small sign that the tide is turning – could unfold over the weekend and cause stocks to soar on Monday as short-sellers absorb the brunt of the damage. Attaching a meaningful probability to these scenarios may seem futile, but running through the scenarios in one’s head to see what the implications are is certainly worth a little bit of spare brainpower.

Just a few months before the 2011 debt ceiling crisis, there was the three-pronged crisis that hit Japan, combining an earthquake, tsunami and nuclear meltdown. I talked about this crisis in Fukushima Daiichi and Event Theta and even invented a new term, “event theta,” to describe whether the passage of time was a positive or negative development for those with positions in volatility or other instruments.

“As these events unfolded, seemingly like a slow-motion train wreck, I kept asking myself whether time was in favor of or working against the efforts of those who were trying to limit the damage to the nuclear facility and surrounding areas. In other words, was this a positive theta event (time in our favor) or a negative theta event (a fight against the clock.) Not being an expert in the field of nuclear energy and knowing that certain factors could spiral out of control quickly, but also knowing that efforts were underway to stabilize some of the processes in the plant, I was left to guessing whether current efforts were more likely to fall short and result in a vicious cycle or were expected to stem the problem and turn the tide in favor of the rescue team.

Knowing whether this was a positive or negative theta event also has substantial implications for investment strategies. From a hedging perspective, event theta could influence the selection of hedging vehicles, the anticipated timing for those hedges, how the hedges might be structured and what sort of prices might be appropriate. For the speculative investor, event theta can also help to determine the risk-reward payoff structure and how it varies over time. Anyone who trades in VIX futures and deals with the VIX term structure on a daily basis should have some insights into potential mismatches between event theta and term structure.”

I suspect that for most of this week, event theta has been negative, meaning that the passage of time without meaningful progress toward an agreement was bearish for equities and bullish for holders of long volatility positions. With the weekend coming up and another two plus days of the news cycle, polling data and behind-the-scenes strategizing, it may be that event theta is closer to neutral and perhaps even positive. This is not to say that shorts should cover their positions before today’s close or anyone with a long volatility position should close out their positions and take profits, only to point out that at least until markets open again on Monday, risk for longs and shorts is becoming more balanced and determining the risk-reward payoff for a variety of positions is a much more difficult proposition.

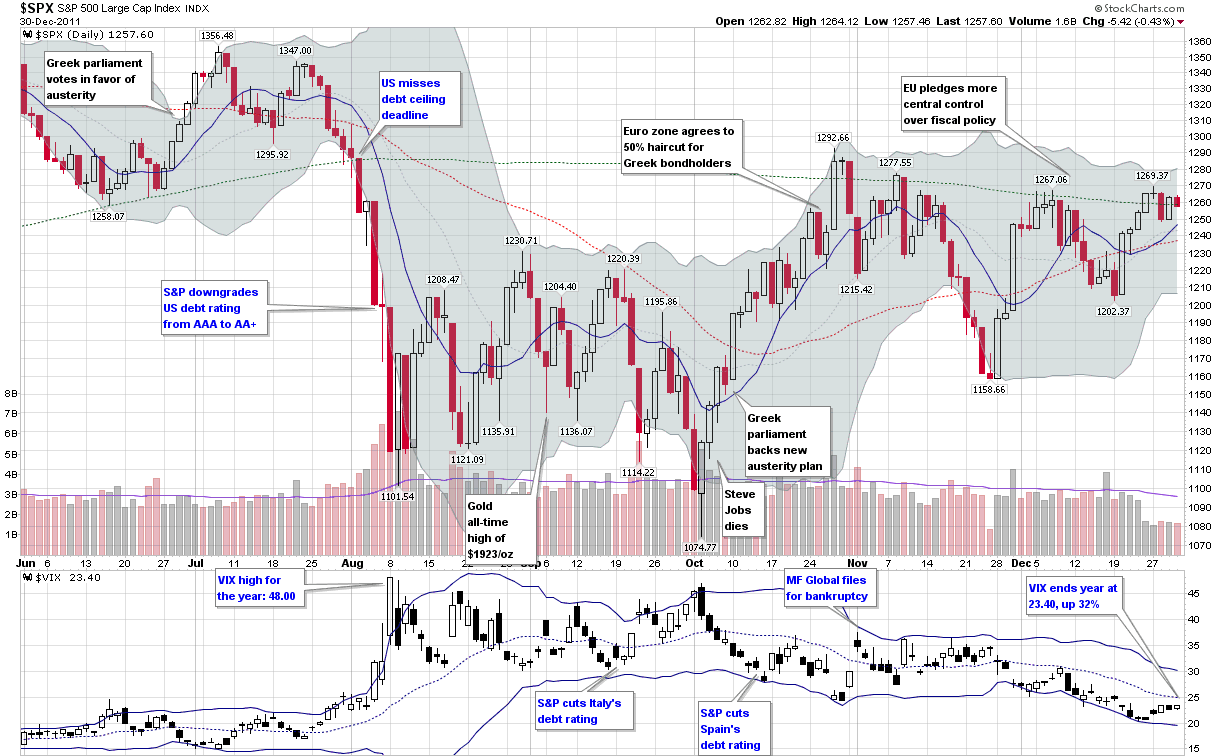

Before the weekend is upon us, investors may wish to give some thought to the 2011 debt ceiling crisis, the 2012 sequestration battle and the timeline for how the 2013 deadlock might play out. In the meantime the, graphic below [an excerpt from The Year in VIX and Volatility (2011)] and the links below that should provide some food for thought about these and a number of related issues.

[source(s): StockCharts.com, VIX and More]

Related posts:

- Volatility During Crises

- Fukushima Daiichi and Event Theta

- The Year in VIX and Volatility (2011)

- Availability Bias and Disaster Imprinting

- Just a Change of Venue? (Fears of Deficit/Debt Ceiling Replacing Fiscal Cliff Worries)

- The Biggest VIX Spike Ever: A Retrospective

- Highest Intraday VIX Readings

- Short-Term and Long-Term Implications of the 30% VIX Spike

- VIX Spike of 35% in Four Days Is Short-Term Buy Signal

- Lessons from the Post-2/27 VIX Price Action

- VXO Chart from 1987-1988 and Explanation of VIX vs. VXO

- Volatility History Lesson: 1987

- Forces Acting on the VIX

- A Conceptual Framework for Volatility Events

- How to Trade Options Around Volatile Events (Barron’s)

- Be Greedy While Others Are Fearful (Barron’s)

Disclosure(s): none