BP, Put Backspreads and the Disaster Trade

One of the more interesting trading setups is something I call the disaster trade. This type of trade typically sets up after a stock experiences a crushing blow, crashes once or twice and has shorts swirling all around it betting that the company will either fail or become permanently crippled.

This is exactly the type of situation BP is currently experiencing.

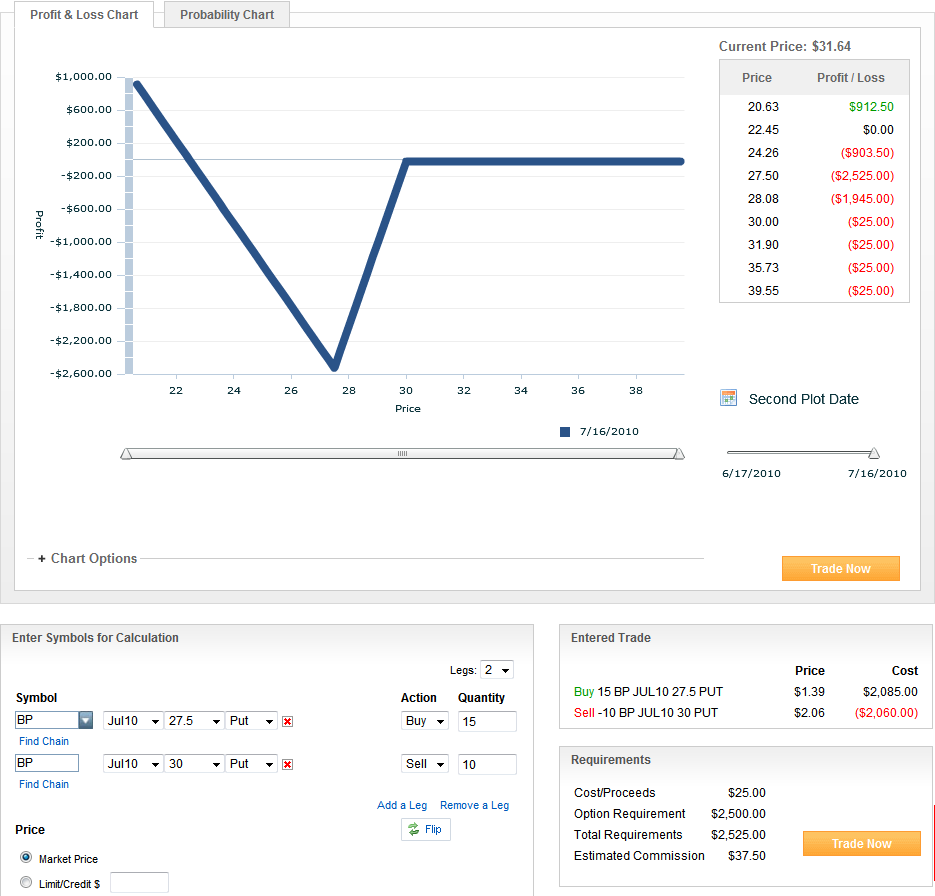

One different sort of way to use options to try to capitalize on the BP situation with limited risk is through the use of a put backspread or a call backspread. A put backspread involves selling a smaller quantity of puts at a higher strike and buying a larger amount of puts at a lower strike. Depending upon market factors, this trade can be either a credit or a debit. In the first graphic below, the trade costs $25 to enter (before commissions.)

The optionsXpress graphics below illustrate the logic of a put backspread trade, which was mapped out with BP trading at 31.64 and is structured here as short 10 BP July 30 puts and long 15 BP July 27.50 puts. From a high level perspective, three things can happen with this trade:

- If BP remains above 30, then the trader loses the $25

- If BP falls below 22.45, the trade begins to make money at the rate of $500 per point

- The trade loses money if BP settles in the 22.45 – 30.00 range, with a maximum loss of $2525 at 27.50

In sum, a disaster pays off; a mild decline will be painful; and any move up, sideways or slightly down move just about breaks even. (In this case the 15:10 ratio means a $25 loss, but if the ratio were smaller, the sideways to up move would result in a profit. For example, buying 14 July 27.50 puts instead of 15 increases the profitability by $139, so any close over 30 would result in a $114 profit instead of a $25 loss.)

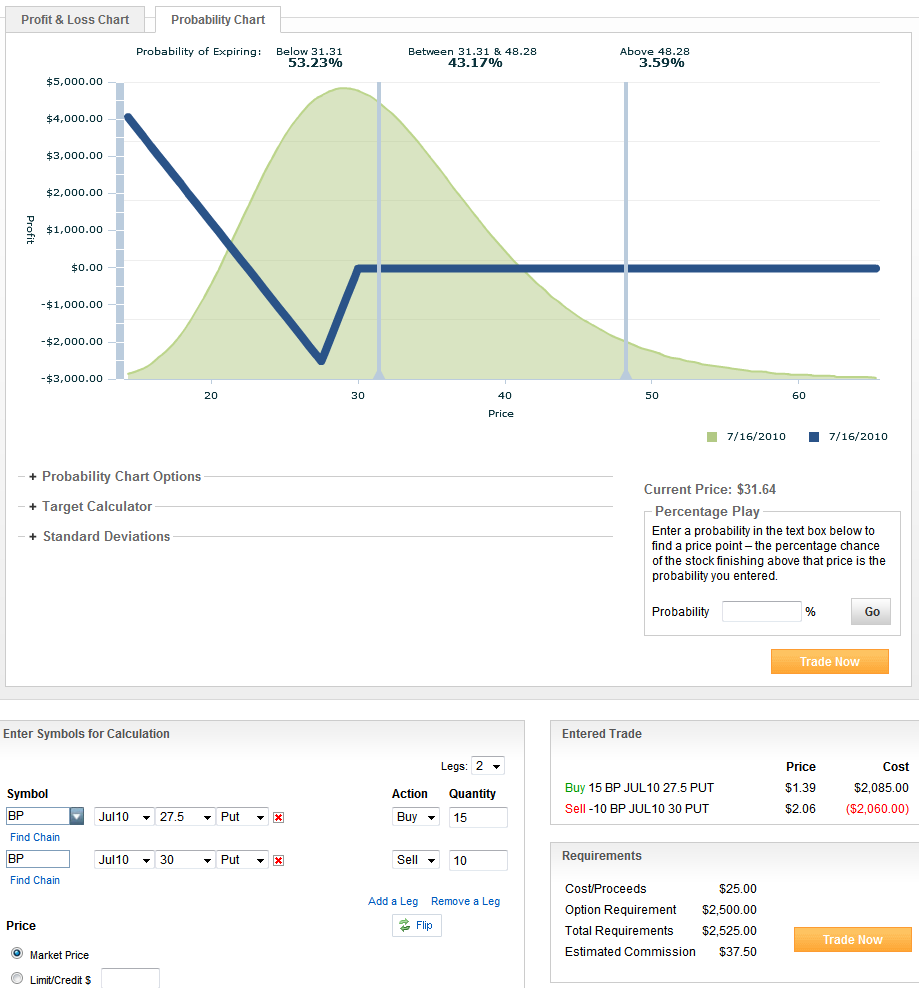

I have included the second graphic to show how optionsXpress uses a lognormal distribution to translate existing options data into an expected probability distribution at the time the July options expire. This helps to visualize the strategy and reinforces the fact that the put backspread is a fat tail disaster play.

Of course, one could flip these graphics around and have a call backspread trade, such as short 10 July 32 calls and long 15 July 35 calls. Here the small profit (about $700 in the example immediately above) would be on the down side and the upward sloping portion of the profit curve would be consistent with a rally instead of a crash.

If you see a beaten down stock that you expect to bounce back strongly, yet still want to make money if the stock continues to sell off, put backspreads are worth investigating. The can be done with out-of-the-money options, as is the case with the examples shown here, using in-the-money-options or with a blend of the two. More broadly, when disaster strikes and you want to place a bet on the situation worsening or improving, backspreads are an interesting way to do so with a defined risk approach.

For more on related subjects, readers are encouraged to check out:

[source: optionsXpress]

Disclosure(s): none