Was the VIX Too Low in 2013? No…

There was a time when investors would generally fret about the VIX being “too high” and the resulting possibility that there was some sort of unseen threat to the financial markets that was not showing up on their radar. In the last few years, the situation has reversed and now I find investors expressing more concern about a low VIX more often than a high VIX. Yes, there are some (many, actually) who start to get anxious and fearful when the markets are not reflecting as much anxiety and fear as they think they should. For those who still think about the battle scars from 2008, this phenomenon seems to be a recurring issue. (See my posts on disaster imprinting for more information on this.)

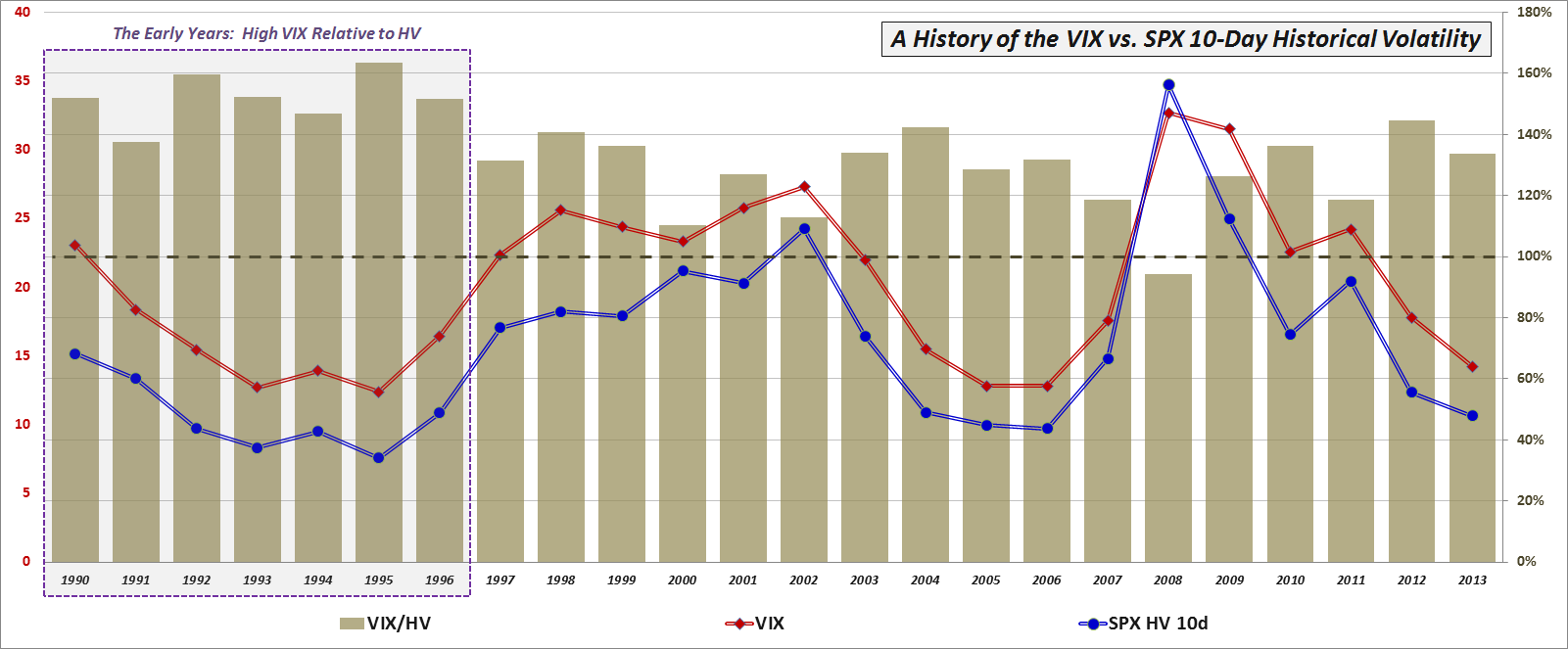

So…was the VIX too low in 2013? In order to answer this question, I am updating a chart I last presented in October 2012 in Ratio of VIX to Realized Volatility Higher than Any Year Since 1996.

As the chart shows, both the (mean) VIX and 10-day historical volatility (HV) of the S&P 500 index were are relatively low levels during 2013. More importantly, the VIX maintained an average premium of 34% to the 10-day HV of the SPX during the year, which is right in line with historical norms going back to 1990 of a premium of about 35%.

[source(s): CBOE, Yahoo]

While I have used data provided by the CBOE going back to 1990 in calculating historical norms, I think it is worth noting that from 1990-1996, the VIX typically had a much higher premium relative to historical volatility in the SPX than it has in more recent years, so whereas the long-term VIX premium to HV stands at about 35%, the post-1996 average premium is closer to 26%. As a result, if you really need to drive home the point that the VIX was “too low” in 2013, you can always trot out the post-1996 data, but otherwise consider the VIX to be just about exactly where it should have been – at least in relation to historical volatility – during the past year.

Last but not least, the chart also illustrates that while the VIX and SPX HV do have a tendency to trend over the course of several years, the ratio of the two has a much more random movement and is therefore much more difficult to predict for 2014.

Related posts:

- Volatility During Crises

- Ratio of VIX to Realized Volatility Higher than Any Year Since 1996

- VIX Premium to Historical Volatility at Record High in Q1

- S&P 500 Index 20-Day Historical Volatility Hits 39-Year Low

- VIX and Historical Volatility Settling Back into Normal Range

- Chart of the Week: No More Free Lunch for Volatility Sellers?

- The Gap Between the VIX and Realized Volatility

- What Is Historical Volatility?

- Rule of 16 and VIX of 40

- Availability Bias and Disaster Imprinting

- VIX Data to Support Availability Bias and Disaster Imprinting Hypothesis

- Calculating Centered and Non-Centered Historical Volatility

- Thinking About Volatility (First in a Series)

Disclosure(s): CBOE is an advertiser on VIX and More