VXX Premium to Indicative Value Falls Slightly to 26%

It has been two weeks since Barclays surprised volatility investors by announcing the suspension of new creation units in the popular iPath Series B S&P 500® VIX Short-Term Futures ETN (VXX). Yesterday, a Barclays press release clarified some of what happened, noting that the firm had issued $15.2 billion more in VXX than had been authorized in an August 2019 $20.2 billion shelf registration. Barclays has elected to conduct a rescission offer to eligible purchasers and is also dealing with regulatory authorities on this matter.

As for the future of VXX, Barclays was vague, but ended their press release

with the following statement:

“Barclays intends to file a new automatic shelf registration statement with the SEC as soon as practicable. Barclays remains committed to its structured products business in the United States.”

It is worth noting that VXX is a small part of the $12.7 billion structured products business in the United States that Barclays has pledged to continue with. In that respect, the future of VXX is uncertain, but the intent to file a new automatic shelf registration “as soon as practicable” is certainly a favorable development.

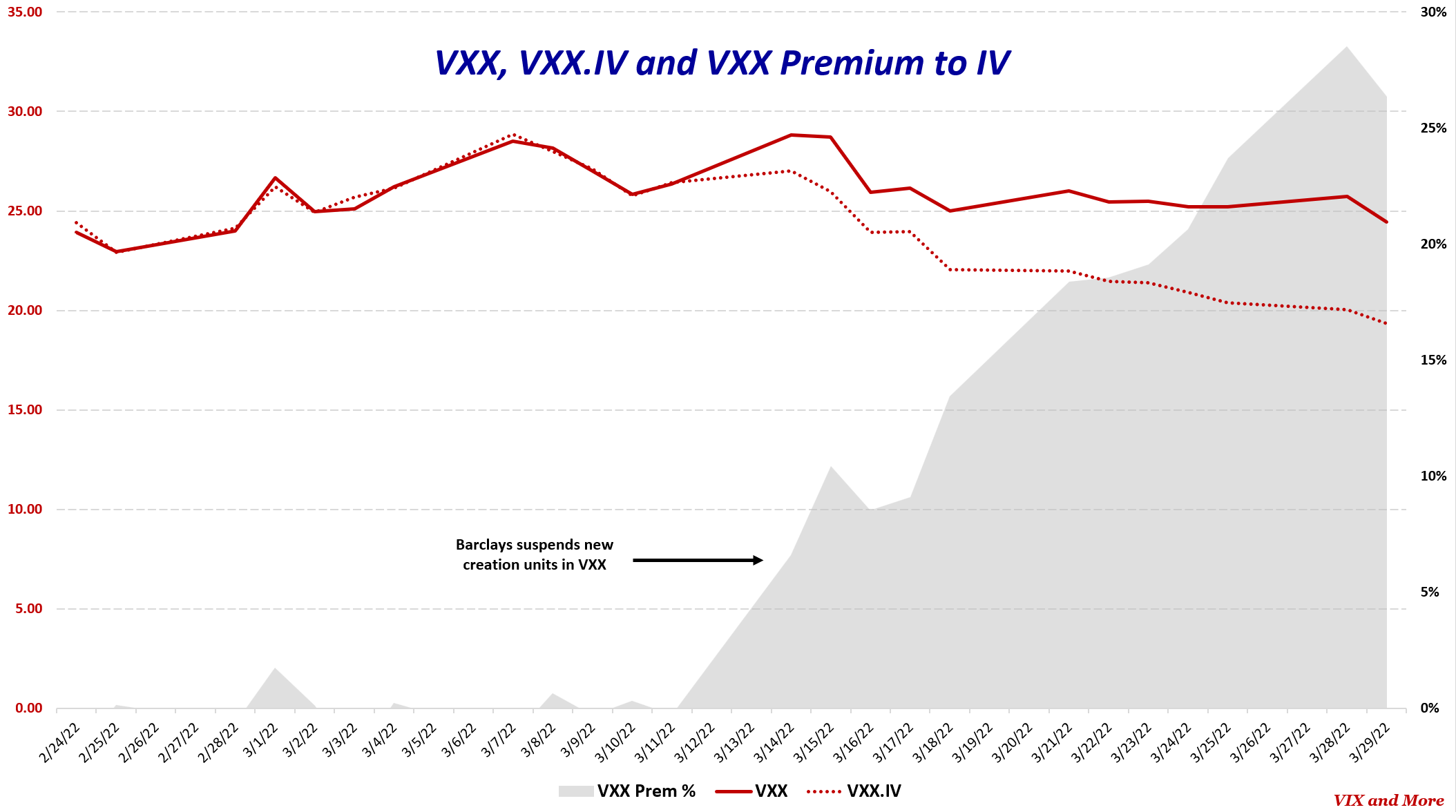

VXX is down today with positive developments in the talks between Russia and Ukraine, but for the first time since March 16th, the VXX premium relative to its intraday indicative value (IV) is down from the previous day, currently at 26.3%, down from yesterday’s 28.5% at the close.

The chart below captures the journey in VXX relative to indicative value (VXX.IV) going back to the Russian invasion of Ukraine.

As noted previously, the risk for shorts is that the short squeeze will continue and maybe even accelerate, perhaps in dramatic fashion, with the VXX premium to VXX.IV rising sharply. On the other hand, the risk for longs is that Barclays will suddenly announce a new automatic shelf registration and the premium to IV will suddenly collapse to zero, as was the case with TVIX and Credit Suisse back in 2012.

While options in VXX are expensive (implied volatility is at 120), defined risk options trades are typically the best way to proceed when there is substantial “jump risk” (or overnight gap up or gap down risk) in both directions.

Finally – and for

completeness sake – I should note that the OIL ETN that also had

its creation units suspended in conjunction with VXX continues to behave relative

to its indicative value, currently showing a premium of just 0.05 over

indicative value.

[source(s): TD Ameritrade]

Further

Reading:

VXX

Upside vs. Downside Risk with No New Creation Units

Barclays

Suspends Creation Units for VXX

Attempt

at TVIX Short Squeeze Fizzling Out

The

Resurrection of TVIX

TVIX

Premium to Indicative Value Creeping Back Up

TVIX

Creation Units Return; What It Means for Investors

Is

TVIX Now Just a More Docile UVXY?

Recent

TVIX Volume and VIX Futures Volume

The

Story of VIX ETPs Relative to their Intraday Indicative Values

The

Ups and Downs of the New Premium in TVIX

Credit

Suisse Suspends Creation Units in TVIX: What it Means

Four

Key Drivers of the Price of TVIX

Will

TVIX Go to Zero?

Who Is

Trading TVIX?

Volatility

Becomes Unhinged on Friday

TVIX

Finally Getting Its Due As Day Trading Rocket Fuel

All About

UVXY

While it has not

been updated in a while, new readers may also enjoy older posts that have been

tagged with the Hall of

Fame label.

For those who may be interested, you can always follow me on Twitter at @VIXandMore

Disclosure(s): net short VXX at time of writing