A reader notes:

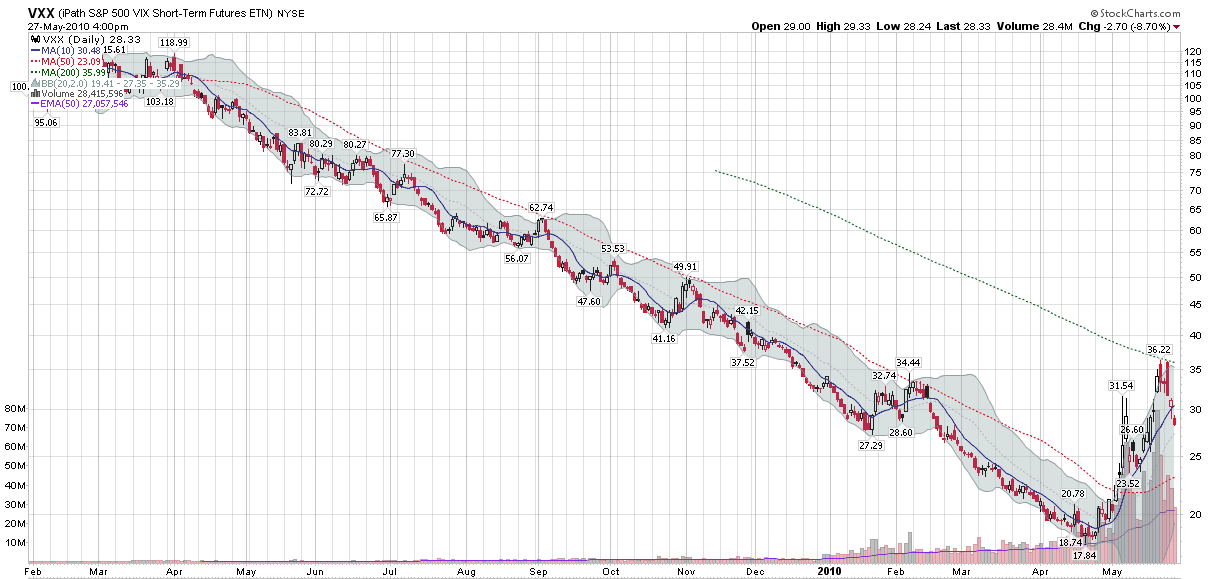

The VIX tends to move inversely with the market on a day-to-day basis. Market up = VIX down and market down = VIX up. That’s all fine and dandy MOST of the time (I’m stating the obvious here) because of expectations about the asymmetry of volatility during bull versus bear moves. But how do we square moves like Monday (05/17) when, even though the close-to-close change in the market was very small, the intraday move was very large (with implications re: continued high volatility), yet the VIX still fell? Does the VIX (from a statistical correlation perspective) only care about close-to-close changes? Isn’t that a bit shallow?

This is an excellent comment and set of questions.

In terms of background, consider that measures of volatility based on actual changes in the price of the underlying break out into two camps:

- those that focus on close-to-close price changes and ignore/understate intraday price movements (e.g., historical volatility)

- those that include intraday price variations in their calculations (e.g., average true range)

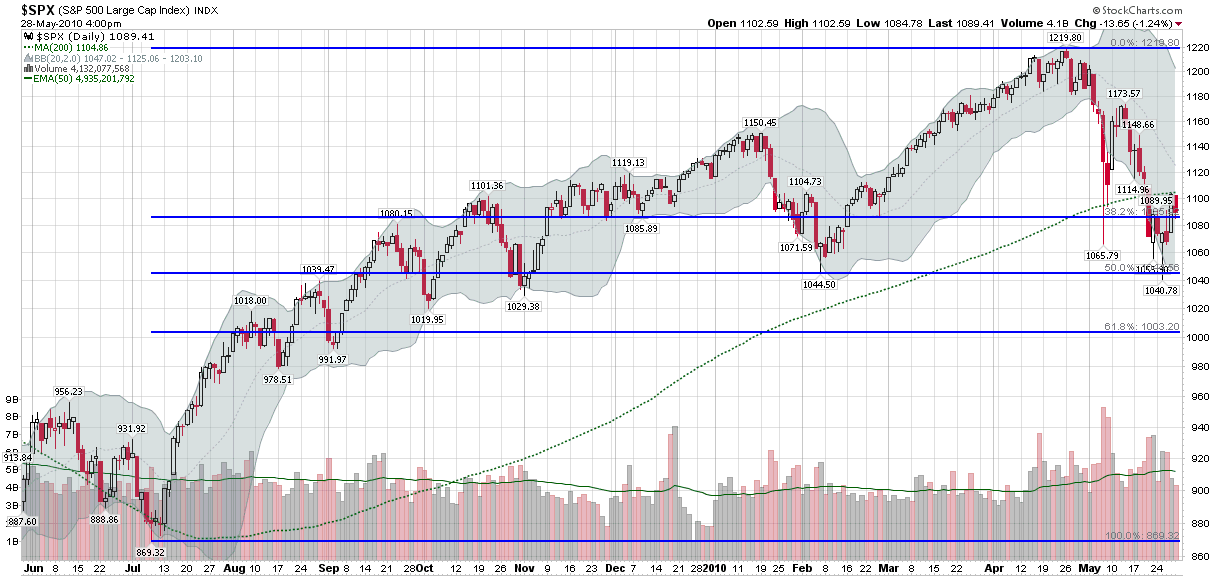

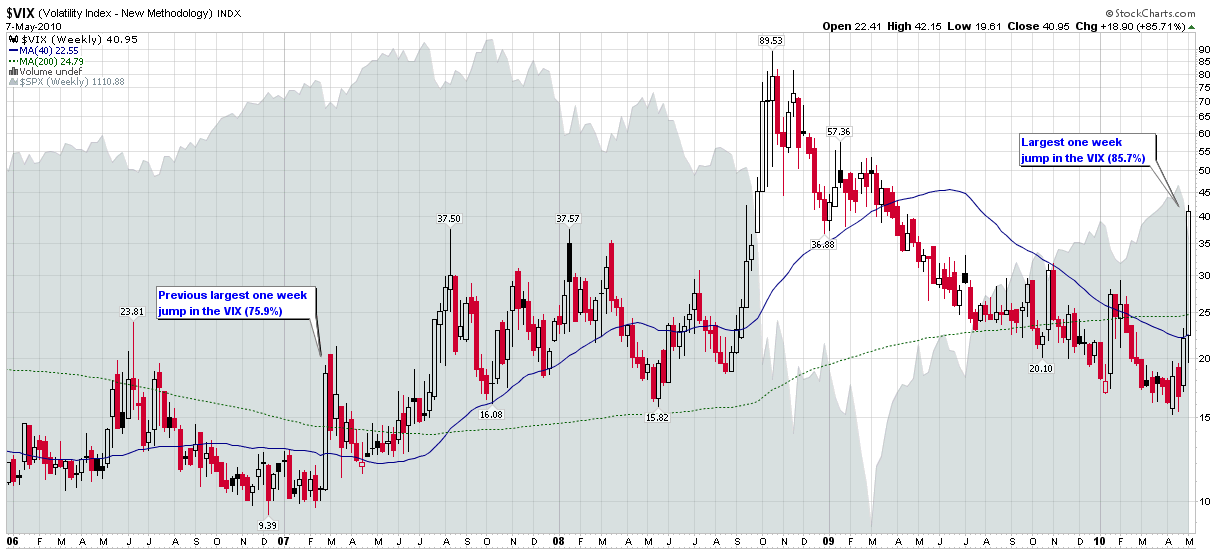

Here is where an example might help to clarify things. Take the recent ‘

flash crash’ of May 6

th. Even though the close-to-close change in the S&P 500 index (SPX) was a very large 3.24%, the intraday range was a whopping 8.73%. So which was the better measure of volatility on that day? My guess is that anyone who was watching the markets as they crashed would vote for the 8.73% move, as things certainly felt more like the panic of October 2008 than the relative calm of October 2007.

Given that implied volatility values such as the VIX are calculated directly from options prices, in theory the VIX does not strictly account for intraday prices. Also, technically the VIX is the market's forward estimate of close-to-close volatility in the SPX. So from a pure statistical perspective, the VIX does indeed have a narrow close-to-close time horizon and is blind to intraday fluctuations in prices.

In practice, however, a wide range day with a relatively benign close-to-close number will typically reinforce the idea that the market is ripe for large volatility moves, even if these moves may cancel each other out on intraday basis. In my opinion, mapping these changes in price to changes in volatility is where fundamental factors and path dependency come into play. If stocks go up 3% intraday, for example, then fall back to even due to news that, say, the government had to prop up a U.K. bank,

Spain has announced it will not implement austerity measures, a Fed member makes a speech in which he or she suggests interest rate hikes are coming soon, there is a terrorist attack in Israel, etc., you would expect to see the VIX price in more volatility in the next 30 days. On the other hand, if stocks start the day down 3%, but closed even following news that lots of jobs were created, housing prices are increasing, the euro rallied to 1.30, etc., then I would expect the VIX to price in less volatility in the next 30 days.

In brief, on a wide range day, I would look hard at the fundamentals or what I call the

Forces Acting on the VIX, as well as perhaps the elements of volatility I summarized in

A Conceptual Framework for Volatility Events. If news suggests that an obvious threat to the market has been eliminated or diminished significantly, then I would expect the VIX to fall, depending upon the applicability of the

dragon metaphor. If a new threat crops up or an old one suddenly seems more robust, then I would expect to see a rising VIX.

Even when stocks seem to turn the corner and put a threat behind it, there is often some sort of psychological hangover that behavioral economists would probably call “

availability bias” and I have termed “

disaster imprinting.” This is the type of thing that happens on a wide range day that ends with a neutral close. So while the VIX is really estimating what historical close-to-close volatility will be 30 days hence, the presence of wide intraday moves almost necessarily forces options traders to consider increasing their estimates of the probability and/or magnitude of large market moves going forward.

Finally, getting back to your question about last weekend, part of what happened was that on Friday skittish investors bought so much portfolio insurance that the VIX priced in the possibility of a very large volatility event. When Monday's reality fell short of Friday's worst fears, the VIX began to fall.

For more on related subjects, readers are encouraged to check out:

Disclosure(s): short VIX at time of writing